Data Source: Customs Administration, Ministry of Finance, Taiwan (R.O.C) — Import/Export Statistics

Data Source: Customs Administration, Ministry of Finance, Taiwan (R.O.C) — Import/Export Statistics

Published: June 10, 2026

---

Overview

Taiwan's steel bar import market in January–May 2026 was defined by a clear structural split: alloy steel led, carbon steel lagged.Alloy steel round bar imports surged from March on the back of a restocking wave, holding above 12,000 MT per month through April and May— the primary driver of H1 import momentum. Average alloy prices fell from $809 in January to a trough of $722 in March, then stabilized and recovered to $767 by May. Carbon steel round bar volumes remained depressed throughout the period at a monthly average of roughly 3,774 MT, but average prices — flat at $596–$599 from January through April — bounced to $650 in May, a signal worth watching.

For buyers assessing Q3 market direction, three external variables are critical: the preliminary ruling timeline for South Korea's anti-dumping investigations against Chinese steel bars, the direction of China Steel Corporation's Q3 long-product pricing announcement, and the timing of any post-summer restocking in mainland China once the seasonal slow season ends.

---

1. Volume Overview

1-1 Monthly Import Volume

1-2 Volume and Price Summary

1-2 Volume and Price Summary

---

2. Carbon Steel Round Bar: Volume Down 30%, Price at Five-Year Low

2-1 Monthly Trend

Carbon steel round bar imports totaled 18,869 MT in January–May, down 30% year-over-year. The average CIF price of $607/MT is the lowest level since 2021.

Monthly volumes were relatively flat, ranging between 2,800 and 4,900 MT. There was no concentrated restocking event comparable to March 2025 (8,859 MT). May's average price of $650 was the only month to recover above $600 during the period.

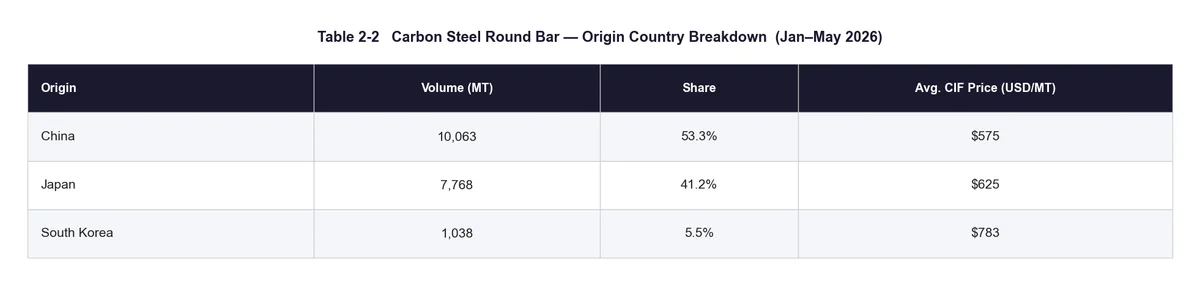

2-2 Origin Country Breakdown

Key observations:

- China and Japan together account for 94.5% of imports — a highly concentrated supply base.

- China's average price of $575 holds at 2025's year-end level. Japan's $625 is only 9% above China, a sharp narrowing from the $216 gap recorded in 2025 ($791 vs $575), indicating Japan is aggressively pricing to defend volume.

- South Korea holds a modest 5.5% share at $783 average — too expensive to expand meaningfully in the near term.

---

3. Alloy Steel Round Bar: March Surge Lifts Total Volume, Prices Still Falling

3-1 Monthly Trend

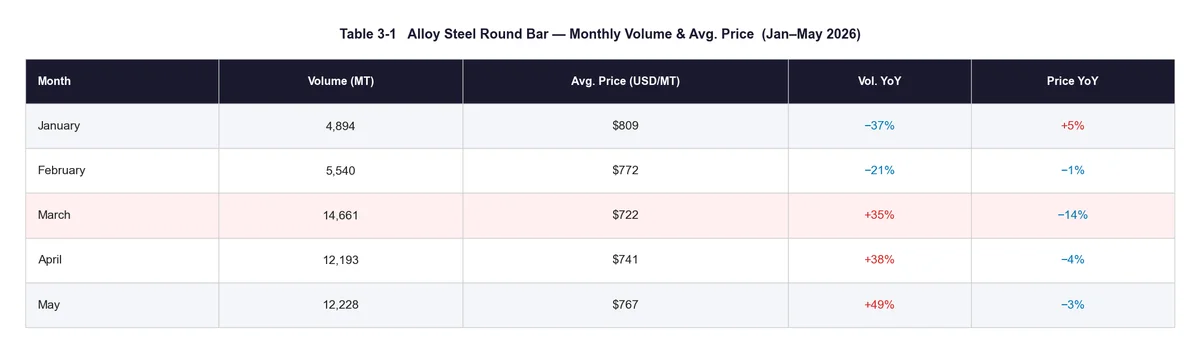

Alloy steel round bar imports totaled 49,515 MT for January–May, up 16% year-over-year. March alone accounted for 14,661 MT — 1.35× the same month last year — attributed to a restocking wave following delayed orders during the Lunar New Year shutdown in January–February.

April–May volumes held above 12,000 MT each month, suggesting restocking momentum had not fully unwound.

> The pattern forms a clear three-phase sequence: trough (Jan–Feb) → surge (Mar) → sustained high (Apr–May).

3-2 Origin Country Breakdown

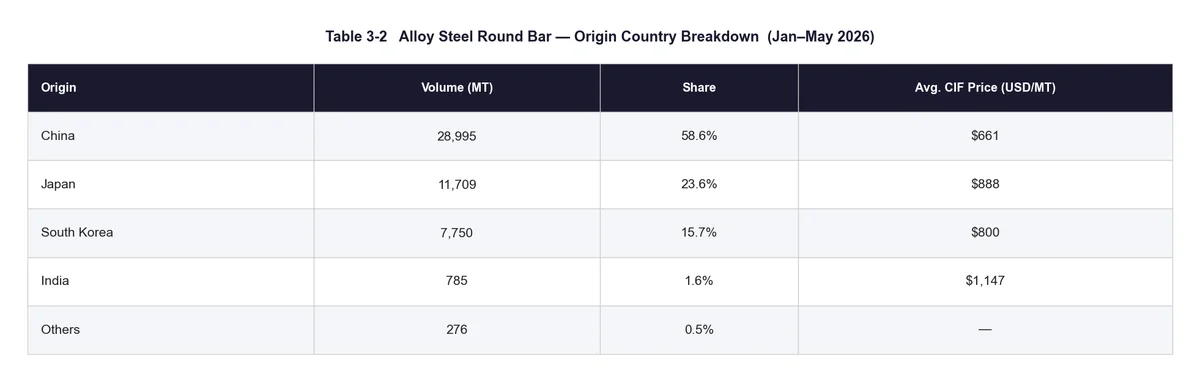

Key observations:

- China maintains dominance at 58.6% share with the lowest average price of $661.

- South Korea's share surged to 15.7%, up sharply from 10% for full-year 2025 — the most notable structural shift in 2026 so far. At $800 average, Korea sits between China and Japan on price, offering buyers an alternative when the China–Japan spread is wide.

- Japan averages $888, a $227 premium over China (34%). Its share of 23.6% slipped slightly from 27% in 2025.

---

4. Market Intelligence: Three External Variables

4-1 South Korea's Anti-Dumping Investigations against Chinese Steel Bars

In May 2026, the Korea Trade Commission (KTC) initiated a series of anti-dumping cases covering multiple Chinese steel bar categories:

Petitioners: SeAH Besteel and SeAH Changwon Integrated Special Steel (combined annual capacity ~3 million MT). Named Chinese respondents include Baowu Steel, CITIC Special Steel, Dongbei Special Steel, and others.

Petitioners: SeAH Besteel and SeAH Changwon Integrated Special Steel (combined annual capacity ~3 million MT). Named Chinese respondents include Baowu Steel, CITIC Special Steel, Dongbei Special Steel, and others.

Potential impact on Taiwan:

- South Korea is Taiwan's third-largest alloy steel round bar supplier (15.7% share in Jan–May 2026). If duties are imposed following a positive preliminary ruling, Korean steelmakers will reduce purchases from China — and some Chinese bar tonnage may be redirected to Taiwan and other markets at discounted prices, adding further downward pressure on import prices.

- The investigations cover HS 7214, 7215, and 7228 — both carbon and alloy steel round bars fall within scope. Preliminary rulings are expected in August–September 2026. Close monitoring is advised.

4-2 Taiwan EAF Mill Pricing

In late May 2026, Feng Hsin Steel and Weich'uan Steel both announced price unchange for their Round 505 wire-rod contracts, ending three consecutive months of increases (Rounds 502–504 cumulative increase: NTD 2,300/MT).

Feng Hsin's investor briefing (2026-05-24) noted that Q1 wire-rod performance exceeded expectations, Q2 momentum continues, but Q3 is expected to be flat-to-firm due to scheduled maintenance and the traditional slow season. Rising summer electricity costs and moderate downstream demand prevented further price hikes.

Watch point: China Steel Corporation's Q3 long-product pricing round is scheduled for announcement in late June and will serve as a benchmark for the broader market.

4-3 Mainland China Steel Market Conditions

China's steel market entered its traditional summer slow season in April–June 2026, with demand softening noticeably:

Early May saw a brief rally on infrastructure restart and iron ore hitting a 22-month high. By June, however, plum-rain season in southern China and high temperatures in the north suppressed construction activity. Social inventories began rising again and prices retreated.

Impact on Taiwan imports: Soft Chinese prices benefit Taiwanese buyers negotiating Q3 forward contracts. However, a potential restocking wave in July–August could trigger a rapid price rebound — buyers should consider locking in some volume at current levels.

---

5. Outlook and Key Indicators

5-1 Carbon Steel Round Bar

Current state: volume contraction and price rebounded from the bottom; weak demand signal.

Average monthly imports in January–May 2026 were approximately 3,774 MT — only 80% of the full-year 2025 monthly average of 4,691 MT. The average price of $607 is at a near five-year low, with both China and Japan cutting prices to compete on volume (Japan's $625 average is near a recent low).

Near-term outlook remains cautious. If downstream demand has not absorbed the March surge inventory, June marks the entry into a genuine off-season. The China Steel Q3 long-product pricing announcement will provide a new reference point.

5-2 Alloy Steel Round Bar

Current state: volume gains are restocking-driven; prices in structural decline.

April–May volumes above 12,000 MT each month confirm restocking momentum persists, but the average price of $752 is at a three-year low with every month below $810. China's $661 average is approaching historical lows. A break below average price would substantially pressure Japanese and Korean suppliers and could accelerate Japan's shift toward higher-grade, differentiated product strategies.

South Korea's sharp market-share gain to 15.7% (a four-year high) warrants monitoring: it is unclear whether Seoul can sustain export volumes to Taiwan during its own domestic anti-dumping proceedings against Chinese bars.

5-3 Three Key Indicators to Watch

---

6. Conclusion

H1 2026 in Taiwan's steel bar import market is defined by a clear split: carbon steel round bars contracting in both volume and price, while alloy steel round bars post a volume gain that masks sustained average-price erosion. Chinese suppliers hold their market position through aggressive pricing, while South Korea's unusual volume surge and Seoul's anti-dumping filings against Beijing are reshaping the regional supply landscape.

Buyers should monitor three near-term developments:

1. Prior to the KTC preliminary ruling (Aug–Sep 2026): watch whether Chinese mills accelerate shipments to Taiwan ahead of potential trade barriers, pushing spot prices toward new lows.

2. China Steel Q3 pricing round: use it as the benchmark for comparing domestic versus imported material costs.

3. Post-March inventory digestion rate: if June–July volumes do not decline meaningfully, restocking demand is structural and prices have a floor; if volumes drop sharply, move early to lock in spot material at cycle lows.

---

Data in this report is derived from the Customs Administration, Ministry of Finance, R.O.C. Exchange rates are monthly average USD/TWD rates. Market intelligence is compiled from publicly available industry reports dated May–June 2026. This report is for informational purposes only and does not constitute purchasing advice or represent a forecast of final market outcomes.

Double Steel— Market Research Department — June 10, 2026

#Double Steel